When it comes to planning for retirement, one of the key factors to consider is the Social Security retirement age. This pivotal age determines when individuals become eligible to start receiving their Social Security benefits. Understanding this age threshold is crucial for anyone navigating the complexities of retirement planning.

What Exactly is the Social Security Retirement Age?

The Social Security retirement age refers to the age at which individuals become eligible to receive full retirement benefits from the Social Security Administration. It is essential to note that this age is not fixed and can vary depending on several factors, including the year of birth. The full retirement age is the age at which individuals are entitled to receive their full Social Security benefits, without any reduction.

Understanding Social Security Retirement Age

Here is some information regarding the retirement age:

- You can get Social Security retirement benefits as early as age 62. However, if you choose to begin receiving benefits before your full retirement age, your benefits will be reduced by a small percentage for each month before reaching full retirement age.

- The full retirement age varies depending on the year you were born. For example, for individuals born in 1960 or later, the full retirement age is 67.

- If you delay taking your benefits beyond your full retirement age, up to age 70, your benefit amount will increase. This is because of delayed retirement credits that are added to your benefit.

- It’s important to note that the full retirement age has gradually increased over the years due to factors such as increased life expectancy and improved health in older age. Congress passed a law in 1983 to raise the full retirement age gradually for individuals born in 1938 or later.

Factors Affecting the Social Security Retirement Age

Several factors come into play when determining the retirement age for an individual:

1. Year of Birth

The year in which a person was born plays a significant role in determining their full retirement age. For example, individuals born before 1938 have a full retirement age of 65, while those born after 1960 have a full retirement age of 67.

2. Early or Delayed Retirement

While individuals can start claiming their Social Security benefits as early as age 62, doing so will result in a reduction in monthly payments. On the other hand, delaying retirement beyond the full retirement age can lead to increased benefits.

3. Spousal Benefits

For married couples, the retirement age can also be influenced by spousal benefits. Spouses may be eligible to claim benefits based on their partner’s work record, further complicating the decision-making process.

Retirement Age Eligibility

Full Retirement Age (FRA)

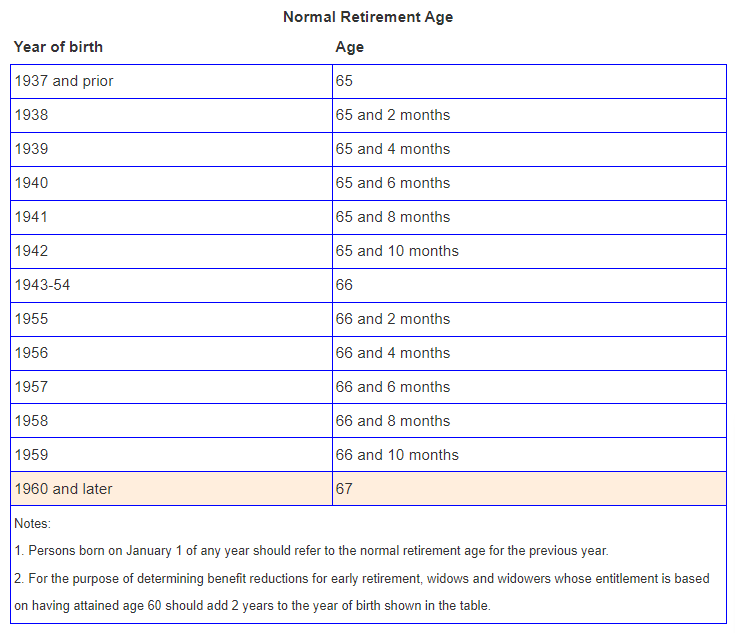

The Full Retirement Age (FRA), also known as Normal Retirement Age (NRA), is the age at which individuals can claim their full Social Security retirement benefits. Historically, the full retirement age was 65 for those born before 1938. However, due to changes in legislation, the full retirement age gradually increased for subsequent birth years.

For individuals born between 1943 and 1954, the full retirement age is 66. It then increases incrementally, reaching 67 for those born in 1960 or later.

FRA is the age when someone can receive full retirement benefits. This age varies depending on the year of birth:

- For those born in 1937 or earlier, the FRA is 65.

- It increases gradually for those born between 1938 and 1959, from 65 and 2 months to 66 and 10 months.

- For individuals born in 1960 or later, the FRA is 67.

Early Retirement

While the full retirement age serves as a benchmark for claiming full benefits, individuals have the option to retire early and start receiving reduced Social Security benefits as early as age 62. However, claiming benefits before reaching full retirement age results in a permanent reduction in monthly payments.

The reduction is calculated as 5/9 of one percent for each month before FRA, up to 36 months. If retirement starts more than 36 months before FRA, the benefit is further reduced by 5/12 of one percent per month.

Delayed Retirement Credits (DRCs)

Conversely, individuals can choose to delay claiming Social Security benefits beyond their full retirement age. By doing so, they can accrue delayed retirement credits, which increase the amount of their monthly benefits. Delaying benefits can be advantageous for those seeking to maximize their Social Security income in later years.

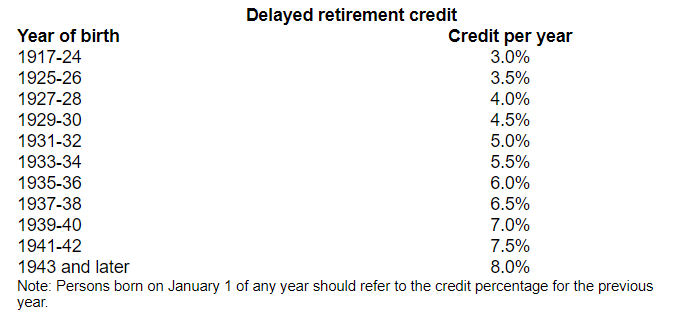

If you delay taking your benefits beyond your FRA, your benefits will increase due to Delayed Retirement Credits (DRCs). The benefit increase ends at age 70.

The annual DRC percentage varies from 3% to 8% by year of birth.

If you were born in 1955, for example, your FRA is 66 and 2 months, and if you start receiving benefits at age 67, you’ll receive 106.7% of the monthly benefit.

Planning for Retirement: Maximizing Social Security Benefits

With the FRA moving to 67 for those born in 1960 or later, individuals may need to adjust their retirement plans accordingly. It’s crucial to consider the timing of benefit claims, as the age at which you decide to claim Social Security is a significant retirement decision.

Given the complexities surrounding the retirement age, strategic planning is essential to maximize benefits. Here are some tips to consider:

1. Delay Claiming Benefits if Possible

Delaying claiming Social Security benefits beyond the full retirement age can result in higher monthly payments. While it may require working longer or relying on other sources of income initially, the long-term financial benefits can be significant.

2. Understand Spousal Benefits

For married couples, understanding the implications of spousal benefits is crucial. Couples should explore different claiming strategies to optimize their combined benefits.

3. Consider Health and Longevity

When deciding when to claim Social Security benefits, individuals should consider their health and life expectancy. While claiming benefits early may seem appealing, it may not be the best option for those expecting a longer lifespan.

Medicare and Social Security

It’s important to sign up for Medicare at age 65, even if you plan to delay your retirement benefits. Tying the decision to sign up for Social Security to Medicare eligibility can lead to permanently reduced benefits if done before reaching FRA.

Legislative Changes and Life Expectancy

The gradual increase in the retirement age from 65 to 67 was enacted by Congress in 1983, as people are living longer and are generally healthier in older age. Life expectancy at birth in 1930 was only 58 for men and 62 for women, but the majority of those reaching adulthood could expect to live to 65 or beyond. Since 1940, the average life expectancy at age 65 has increased by about 5 years.

Conclusion

The Social Security retirement age is a moving target that depends on your year of birth. Understanding the implications of early or delayed retirement on your benefits is essential for making informed decisions about when to claim Social Security.

Navigating the intricacies of the Social Security retirement age is an essential aspect of retirement planning. By understanding the factors that influence this age threshold and implementing strategic planning strategies, individuals can maximize their Social Security benefits and achieve financial security in retirement.

FAQs (Frequently Asked Questions)

What is the current full retirement age?

The current full retirement age is 67 for individuals born in 1960 or later.

Can I retire before the full retirement age?

Yes, you can retire as early as age 62, but doing so will result in reduced Social Security benefits.

Are there any penalties for early retirement?

Yes, retiring before full retirement age results in a permanent reduction in monthly Social Security benefits.

How does delaying retirement affect benefits?

Delaying retirement allows you to accrue delayed retirement credits, increasing the amount of your monthly Social Security benefits.

What happens if I work after reaching full retirement age?

If you work after reaching full retirement age, your Social Security benefits may increase due to additional earnings and contributions.

Source –

- https://www.ssa.gov/benefits/retirement/planner/agereduction.html

- https://www.ssa.gov/oact/progdata/nra.html

- https://www.ssa.gov/oact/quickcalc/early_late.html

- https://www.ssa.gov/benefits/retirement/planner/delayret.html